Back to the Learning Academy.

Overboarding: An Analysis on Toronto Stock Exchange Listed Companies

On The Board | A 4-part series

On The Board is a 4-part series of data-driven insights and analysis based on company research of public companies listed on Toronto Stock Exchange

- Part 1: Overboarding: An Analysis on Toronto Stock Exchange Listed Companies

- Part 2: Sector Analysis of Board Diversity

- Part 3: Diversity of Executive Management Teams

- Part 4: Sustainability at the Board

*Unless otherwise indicated, statistics compiled and provided by MarketIntelWorks On The Board Tracker.

Part 1 | Overboarding: An Analysis on Toronto Stock Exchange (TSX) Listed Companies

The board of directors is a critical asset to a public company. Under the Canadian Business Corporations Act (CBCA), a director has a fiduciary duty to act honestly, in good faith and in the corporation's best interest. A recent addition to the CBCA now provides that, in carrying out their duty to act in the best interests of the corporation, the interests considered by directors and officers may include shareholders, employees, retirees and pensioners, creditors, consumers, governments, the environment, and the long-term interests of the corporation.1 The fiduciary duty has expanded beyond sole consideration to the interests of shareholders. With these added considerations and responsibilities, comes added commitments in both time and energy from directors.

Directors are expected to be stewards of the company's long-term strategy, advisors to the CEO and executive management team, monitors of company performance, and public faces for the company. They need to be able to understand increasingly2 complex businesses, demonstrate technical know-how, deliver effective governance, and generate sustainable long-term performance. Meeting attendance and laser focus are crucial to the director role. The time commitment for a director of a publicly traded company averages 250 hours per year per company or the equivalent of six 40-hour work weeks per year per company.3 Add more hours to this total if the director is chair of the board or is the chair of a committee of the board. In some markets, the role of chair of the board is counted as two directorships because of the time commitment involved.

What is Overboarding?

Overboarding refers to a director who sits on an excessive number of boards. What is considered excessive? Proxy advisory firms ISS and Glass Lewis consider any director who sits on more than five public company boards as being overboarded.4 Institutional investors like BlackRock, Vanguard, Fidelity, and State Street are taking a harder line on overboarding and consider any director who sits on more than four public company boards as being overboarded.5 In the past several years, concerns around overboarding have become a key input for votes against director elections. For example, from July 1, 2020 to June 30, 2021, BlackRock voted against 163 directors at 149 companies in the Americas because of overboarding.6 The ISS Proxy Voting Guidelines for TSX-Listed Companies for 2022 states the following rationale for voting against overboarded directors: "Directors must be able to devote sufficient time and energy to a board in order to be effective representatives of shareholders' (and stakeholders') interests. While the knowledge and experience that come from multiple directorships is highly valued, directors' increasingly complex responsibilities require an increasingly significant time commitment. Directors must balance the insight gained from roles on multiple boards with the ability to sufficiently prepare for, attend, and effectively participate in all of their board and committee meetings.7

The issue of overboarding has been a longstanding one. Robust directors with varied experience and professional expertise underpin properly functioning companies. Directors who serve on multiple boards can have greater perspective, industry and economic knowledge. Companies are looking for directors that can bring prior experience to the table and oftentimes, the same candidates are filling the roles. Couple this with the fact that corporate boards are responding to regulatory, societal, shareholder, and stakeholder demands for more diversity and we can see why there are concerns about overboarding on public company boards. Are TSX-listed company directors being stretched too thin? Let's look at the numbers.

An Analysis of Overboarding for TSX-Listed Companies

In 2014, Deloitte Global introduced a metric known as the stretch factor to measure how many board seats an individual holds in a particular market. The higher the stretch factor, the more seats held by any single director.

A stretch factor of 1 indicates that all board seats in a given sample are held by different women and men, while a stretch factor of 1.3 or greater is considered high.8 As of December 31st 2021, the stretch factor for all issuers listed on TSX was 1.18. The stretch factor for women on TSX-listed company boards was 1.24 and for men it was 1.16. The stretch factors have decreased since 2018 where the stretch factor for women was 1.27 and for men, 1.18. This indicates that companies are indeed casting a wider net to fill their board vacancies but that women are more stretched than men when we look at board directorships.

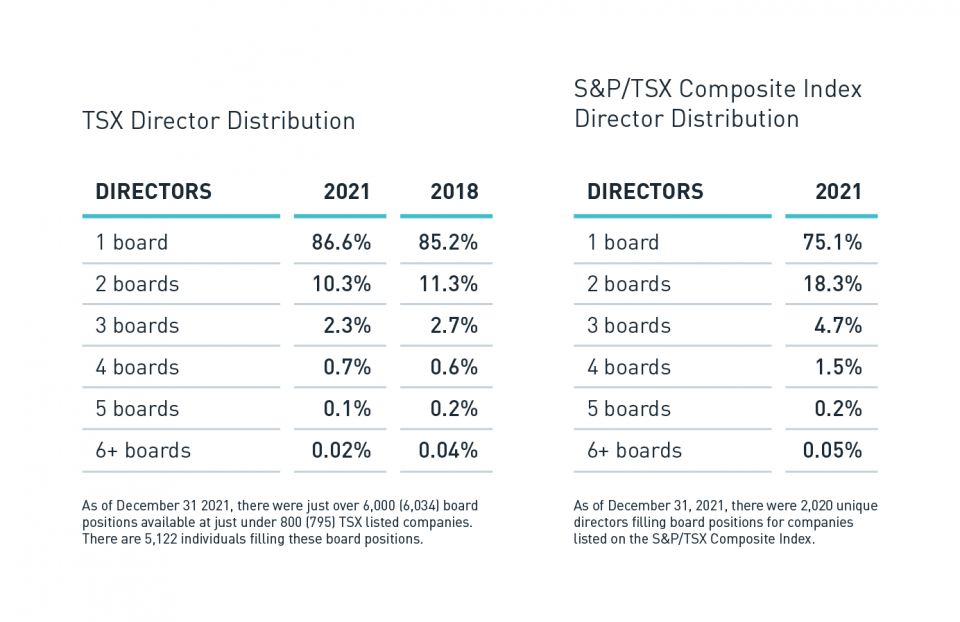

In the entire TSX-listed company universe, 13% of the directors serve on 2 or more TSX-listed company boards. Twenty percent of women directors of TSX companies serve on two or more boards, compared with 12% of men. Ten percent of BIPOC directors are on two or more boards. In the S&P/TSX Composite Index*, 25% of the directors sit on 2 or more boards. Thirty percent of women directors of the S&P/TSX Composite Index companies are on two or more boards, compared with 23% of men. Again, this indicates that women are more stretched than men and that a small pool of women are sitting on multiple boards, especially at the large-cap S&P/TSX Composite Index companies.

Avoiding Overboarding

The dual goal of avoiding overboarding and increasing diversity at the board level can be achieved by creating a rich, large pool of diverse candidates. Combining lists of top corporate women or top BIPOC people, looking at recent graduates of director certification programs, working with recruiters, and looking beyond the C-Suite for board candidates are some ways to increase the pool of diverse candidates. Another way is looking at diverse candidates that are already sitting on one board at a publicly-listed company. There are 900 potential board candidates who are women who currently sit on only one board of a TSX-listed company and there are an additional 1,000 women that are on executive management teams of TSX-listed companies that could also be added into the pool. The same analysis can be done for BIPOC candidates. There are 353 BIPOC candidates who currently sit on only one board and there are an additional 567 BIPOC candidates that are on executive management teams of TSX-listed companies. By tapping larger pools of diverse candidates, there is potential to have more diverse candidates on long lists, then short lists and eventually on the boards of TSX-listed companies.

For related content take a look at the resources below or sign up for our Learning Academy newsletter:

- Going OverBoard podcast

- Setting the Tone from the Top: A Conversation about Diversity on Boards video

- Women in Leadership: Achieving an equal future in a COVID-19 world video

About MarketIntelWorks

Gina Pappano is the Founder of MarketIntelWorks Inc., a data research and analytics company with a focus on gender diversity plus BIPOC (Black, Indigenous, People of Colour) on Boards and Executive Management Teams of TSX listed companies. MarketIntelWorks On The Board Tracker is a comprehensive diversity tracking tool in Canada. Not only do we have the stats with respect to Gender, Visible Minority, Indigenous and Black representation on Boards and Executive Teams, we also have the names of the people behind the stats. Marketintelworks.com

Footnotes

-

Government of Canada. (2022). Canada Business Corporations Act. Version of section from 2019-0621 to 2022-03-07. Retrieved from Justice Laws Website:

https://laws-lois.justice.gc.ca/eng/acts/c-44/section-122-20190621.html

-

Kane, Karen. "Are Board Directors Going Overboard?" Briefings Magazine, Issue no. 31,

https://www.kornferry.com/content/dam/kornferry/docs/article-migration/Briefings31_OTH_OnTheBoard_14-15.pdf

-

Sidley Update. "Roundup of Director Overboarding Policies" October 26, 2021.

https://www.sidley.com/-/media/update-pdfs/2021/10/20211026-roundup-of-director-overboarding-policies.pdf?la=en

-

BlackRock. "Pursuing long-term value for our clients" BlackRock Investment Stewardship A look into the 2020-2021 proxy voting year. Copyright 2021.

https://www.blackrock.com/corporate/literature/publication/2021-voting-spotlight-full-report.pdf

-

ISS. "Canada: Proxy Voting Guidelines for TSX-Listed Companies Benchmark Policy Recommendations" Published December 13, 2021

https://www.issgovernance.com/file/policy/active/americas/Canada-TSX-Voting-Guidelines.pdf

-

Deloitte. "Progress at a snail's pace" Women in the boardroom: A global perspective. Copyright 2022,

https://www2.deloitte.com/content/dam/Deloitte/nl/Documents/AtB/deloitte-nl-women-in-the-boardroom-seventh-edition.pdf

Copyright © 2022 TSX Inc. All rights reserved. Do not copy, distribute, sell or modify this document without TSX Inc.'s prior written consent. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this article, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This article is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. The Future is Yours to See., TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, TSX Venture Exchange, TSXV and Voir le futur. Réaliser l'avenir. are the trademarks of TSX Inc.

* The S&P/TSX Composite Index (the "Index") is the product of S&P Dow Jones Indices LLC or its affiliates ("SPDJI") and TSX Inc. ("TSX"). Standard & Poor's® and S&P® are registered trademarks of Standard & Poor's Financial Services LLC ("S&P"); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC ("Dow Jones"); and TSX® is a registered trademark of TSX. SPDJI, Dow Jones, S&P, their respective affiliates and TSX do not sponsor, endorse, sell or promote any products based on the Index and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions or interruptions of the Index or any data related thereto.

Related Articles